Building a stable financial future is a goal that many individuals aspire to achieve. With the right strategies, anyone can enhance their personal finance knowledge and make informed decisions that will lead to long-term financial stability. Below are essential strategies that can help you on your journey.

1. Create a Comprehensive Budget

A well-structured budget is the cornerstone of effective personal finance management. It allows you to track your income and expenses, helping you identify areas where you can save money. Start by listing all your sources of income and all your fixed and variable expenses. Tools like budgeting apps can simplify this process, enabling you to visualize your financial situation.

Key takeaway: Regularly review and adjust your budget to reflect changes in your financial situation and goals.

2. Build an Emergency Fund

One of the most critical components of personal finance is having an emergency fund. This fund acts as a financial safety net, allowing you to cover unexpected expenses without relying on credit cards or loans. Aim to save at least three to six months' worth of living expenses in a high-yield savings account. This fund will provide peace of mind and financial security.

Key takeaway: Start small if necessary; even saving a small amount regularly can lead to a significant emergency fund over time.

3. Pay Off Debt Strategically

Debt can be a major roadblock to achieving financial stability. Develop a strategy to pay off your debt efficiently. Consider using either the snowball method, where you pay off the smallest debts first to gain momentum, or the avalanche method, where you tackle debts with the highest interest rates first. Prioritizing your debts can save you money on interest and help you become debt-free faster.

Key takeaway: Avoid accumulating more debt by living within your means and using credit responsibly.

4. Invest for the Future

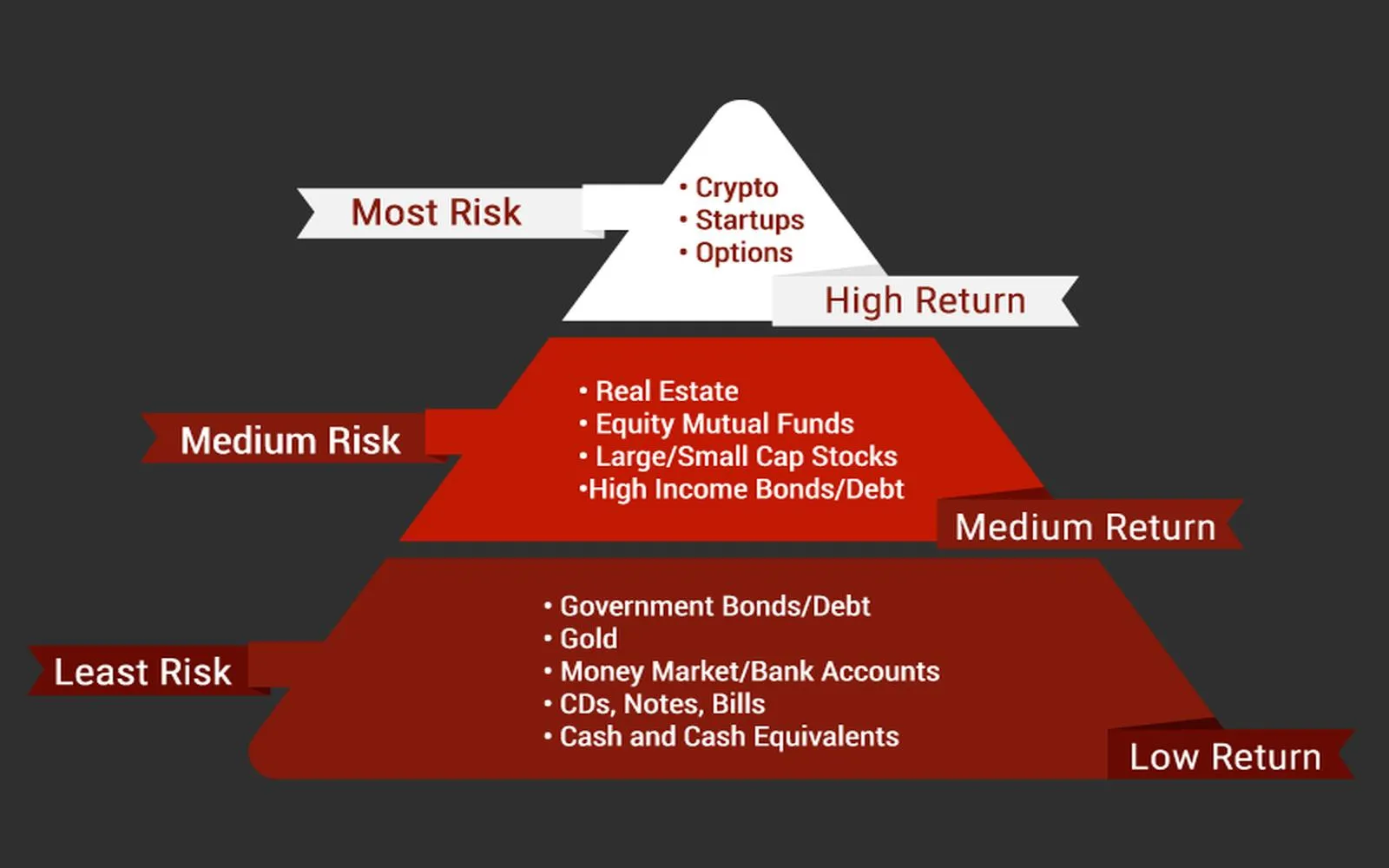

Investing is a crucial aspect of building wealth and securing your financial future. Start by taking advantage of employer-sponsored retirement plans, such as a 401(k), especially if they offer matching contributions. Additionally, consider opening an Individual Retirement Account (IRA) to benefit from tax advantages. Diversifying your investments across stocks, bonds, and other assets can also mitigate risks and enhance returns.

Key takeaway: The earlier you start investing, the more you can benefit from compound interest over time.

5. Educate Yourself About Personal Finance

Knowledge is power when it comes to personal finance. Take the time to educate yourself about financial principles, investment strategies, and money management. There are numerous resources available, including books, podcasts, and online courses. By improving your financial literacy, you can make informed decisions that will positively impact your financial future.

Key takeaway: Stay updated on financial news and trends to make better decisions about your investments and spending.

6. Set Financial Goals

Setting clear financial goals is essential for building a stable financial future. Whether it's saving for a home, funding your children's education, or planning for retirement, having specific targets can motivate you to stay disciplined in your personal finance journey. Break your goals down into short-term and long-term objectives, and create a plan to achieve them.

Key takeaway: Regularly review your goals and adjust them as necessary to reflect changes in your life circumstances.

7. Monitor Your Credit Score

Your credit score plays a vital role in your financial health, affecting your ability to secure loans and favorable interest rates. Regularly check your credit report for errors and take steps to improve your credit score if needed. Pay your bills on time, keep your credit utilization low, and avoid opening too many new accounts at once.

Key takeaway: A good credit score can save you money on loans and insurance premiums.

8. Plan for Retirement

It's never too early to start planning for retirement. Consider how much money you'll need to maintain your desired lifestyle once you stop working. Use retirement calculators to estimate how much you should save each month to reach your goal. Remember to account for inflation and potential healthcare costs in your retirement plan.

Key takeaway: Take advantage of compound interest by starting your retirement savings as early as possible.

Conclusion

Building a stable financial future requires a combination of discipline, knowledge, and strategic planning. By implementing these essential strategies in your personal finance journey, you can work towards financial independence and security. Remember, the key is to stay committed to your goals and continuously educate yourself about the best practices in personal finance.